One of the challenging financial dilemmas everyone faces is budgeting for retirement. This begins early in a career when retirement cannot be fathomed and ends when it is an imminent fact of life. For most people in their working career, retirement planning is little more than periodically adding some money to a tax-sheltered account.

As retirement approaches, we all have the face the reality of our past decisions and future financial needs. Whether you do your own financial planning or hire an expert, in my experience, the most commonly overlooked item in retirement planning is inflation.

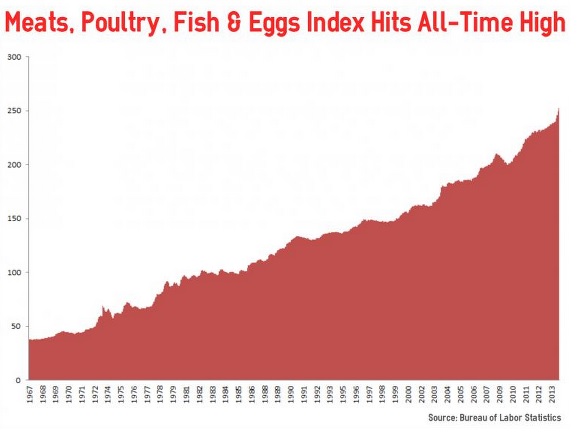

This chart from the U.S. government tracks retail protein sources: beef, poultry, fish, pork, and eggs. From 1967 to 2014, the average annual increase is 4.01%, and it has been fairly steady with any drop proceeded by a new high within a couple years. The impact of this on your budgeting is this: you need to plan for a 4% increase in the price of these items during your retirement. Since the average retirement may last 20 years, as an example, if you spent $1,000 on these proteins in the first year, these would then potentially cost you $4,400 in the 20th year. This reflects the impact of compounding inflation year after year.

This is just one food item that you’ll be budgeting for in your retirement. Yes, some expenses may decline or be eliminated, but many if not most will increase during your retirement. Budgeting is individual, and you can make a rough overall guess at an annual inflation increase; but it is best to examine each of your own expenses. If you don’t want to do that detailed work at least look at your 5 largest expenses to determine if they will likely be going up or down and a rough estimate of how they may change in your future. For example, where I live, property taxes just went up 11% this year and the city just approved an 8% increase in water rates. These increases don’t happen every year, but an increase of some type for these local expenses over any 5-year period is nearly guaranteed.

The important point to consider is to include several inflation rates and spending scenarios in your retirement planning. This will prevent or minimize foreseeable financial problems when you are retired and least able to maneuver for more income.