Financial planners and best-selling gurus all have their pet retirement withdrawal number. This number is the rate at which you withdraw money from your retirement funds to live on for spending money. For example, if you had accumulated $100,000 in your retirement accounts, you would withdraw 5% of the money, or $5,000, to use for spending. Realize that if this money has not yet been taxes then you will also have to pay income tax on this $5,000 withdrawal. Some of the popular withdrawal rate numbers range from 3% (the most conservative) to 12% (the riskiest and Dave Ramsey’s number). Which one is best?

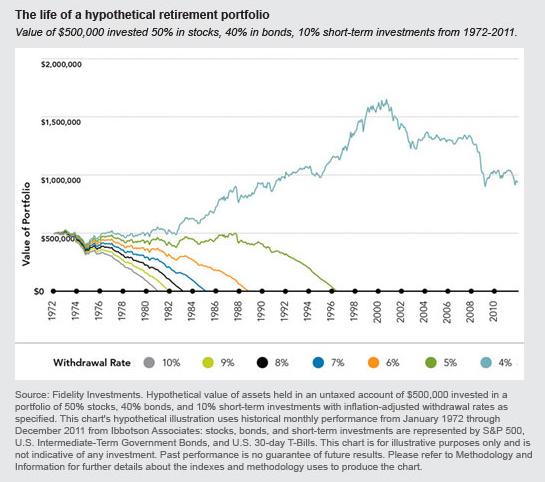

Let’s take a look at the graph to view how these withdrawal rates would have played out using real number from 1972 to 2011 in a study by Fidelity Investments. During this time period, if you were retired, only one withdrawal rate would have allowed your retirement account to survive this period of time – the conservative 4% withdrawal rate.

Understand what this means: if you had withdrawn more than 4% of your retirement money then you would have spent all the money before you passed away – you’d be broke. Actuarial studies show that most people will live 30 to 40 years in retirement. Some pension funds are planning for people to live to 100 years old. This is a long time to survive on money that you saved during your working career. If you run out of money, you are at an age where you are least able to work and earn more money to live on. So if you use a withdrawal rate that is greater than 4%, you are actually planning on a fiscal crash landing – you are planning to be broke too soon!

Do you think it is important to know this number before you stop working? Working just a few more years to save additional money so that you can survive several decades with less financial risk is a great trade-off, even though it may not seem like it at the time.

The likelihood of receiving full social security benefits gets smaller every year with government deficits for decades to come. I do not know how much benefits may be reduced, but even the Social Security Administration predicts that by 2041, retirees may only receive 73% of what they were supposed to get from the program when they were paying into it. This may keep you from starving but probably not a lot more. This is why financial literacy and saving for retirement is more important than ever.